Humanoid Robotics: A Breakdown of The Supply Chain

this serves as a primer to humanoid robotics.

Humanoid robots have been a science-fiction trope for seventy years and a perpetually delayed engineering project for at least thirty. So what changed?

Until 2023, every robot had to be hand-coded for every task. Given the randomness of the physical world, that approach was economically unfeasible. Now, the arrival of vision-language-action (VLA) models as a downstream consequence of the LLM revolution meant that a robot could be told what to do in natural language and figure out the physical motions itself. In fact, the co-evolution of humanoid hardware and software has reached a point where we are beginning to see production ramps necessary for collection of real-world interaction data needed to train the next generation of models.

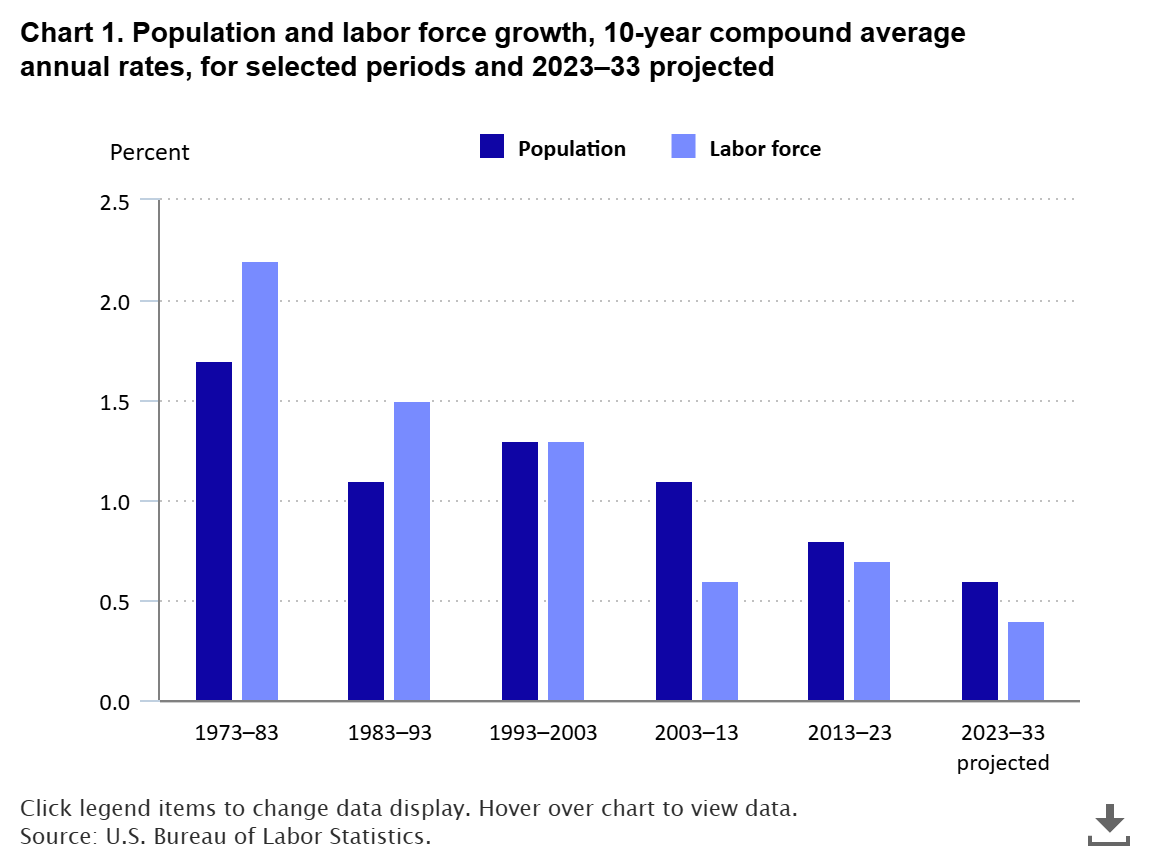

A parallel driver is changes in demographics. G7 and Chinese workforces are aging in lockstep, creating foreseeable labor shortages. In fact, US labor force growth has collapsed from 1.4% pre-2007 to just 0.3% for the US-born workforce, with a projected 6 million worker shortfall by 2032. Reshoring demand from the CHIPS Act and tariff policy is arriving into a labor pool where prime-age participation is already at historical highs. Critically, AI adoption is advancing slowest precisely where physical work is irreducible: manufacturing, logistics, construction, and healthcare. That is the gap humanoid companies are all rushing to fill.

But why make them look human at all? A robot arm on wheels would probably be faster and easier to mass produce. The argument for humanoid form really boils down to how the world is already built for humans. Door handles are at human height, stairs have human-sized steps, tools have human-sized grips, cars have pedals and steering wheels positioned for human bodies, factories have workstations designed for someone roughly 5’8” with two arms. Building a robot that fits that envelope means that you can deploy it anywhere without retrofitting the environment. A wheeled arm can’t climb stairs, can’t step over a curb, can’t fit into a bathroom designed for a human. The humanoid form factor is a bet that general-purpose physical labor is a larger market than the sum of all specialized robotics.

While there may still be some reservations about the feasibility of humanoid robots, the capital has already voted. Global humanoid venture funding year-to-date already exceeds the entirety of 2025, with China contributing roughly 46% of that flow. Apptronik raised $520M at a $5B valuation in February 2026, backed by Google and Mercedes. Tesla has guided to ~$25B in 2026 capex with Optimus production lines explicitly inside that envelope, and Optimus V3 entered small-scale trial production this May with mass-production supplier orders expected in July. Figure just released a video showcasing 2 of their Figure robots autonomously working together to tidy up a bedroom. The point is, whether you believe the long-run vision or not, the question of whether humanoid robots will exist as a real industry has already been settled.

Morgan Stanley’s Thought Experiment

Morgan Stanley’s Global Humanoid Model is, by their own framing, a 25-year forecast.

In my opinion, any 25-year forecast is closer to a thought experiment than a prediction but it nonetheless deserves consideration as the shape of the bet is what matters:

$5 trillion annual market by 2050, including hardware, software, services, and supply-chain infrastructure.

~1 billion humanoid units in service by 2050, with adoption hitting 24.4M units by 2036 and 137.9M by 2040.

ASP curve: from ~$200,000 today in wealthy countries to ~$50,000–$75,000 by mid-century, and as low as $15,000–$21,000 in markets served by Chinese supply chains.

Substitution lens: against a $40 trillion global labor pool (4 billion workers × $10K average), even partial penetration is multi-trillion-dollar.

Tracking signal: Morgan Stanley’s “Humanoid 100” equal-weighted index is up 45% since launch in February 2025, beating the S&P 500, MSCI Europe, and MSCI China.

As I’ve said nobody knows what is going to happen in 25 years. Even then, there is an asymmetric uncertainty skewed positive that makes being early to humanoid robots a good bet. If Morgan Stanley is wrong by 80%, the market is still a trillion dollars. If they are wrong by a wider margin, the downside is bounded by real industrial deployments already happening which even in a pessimistic world, forms a $50–100B niche industrial tool industry by 2050. The upside is a general-purpose labor platform that infiltrates manufacturing, logistics, healthcare, and households. Asymmetric uncertainty skewed positive is precisely the condition that rewards being early.

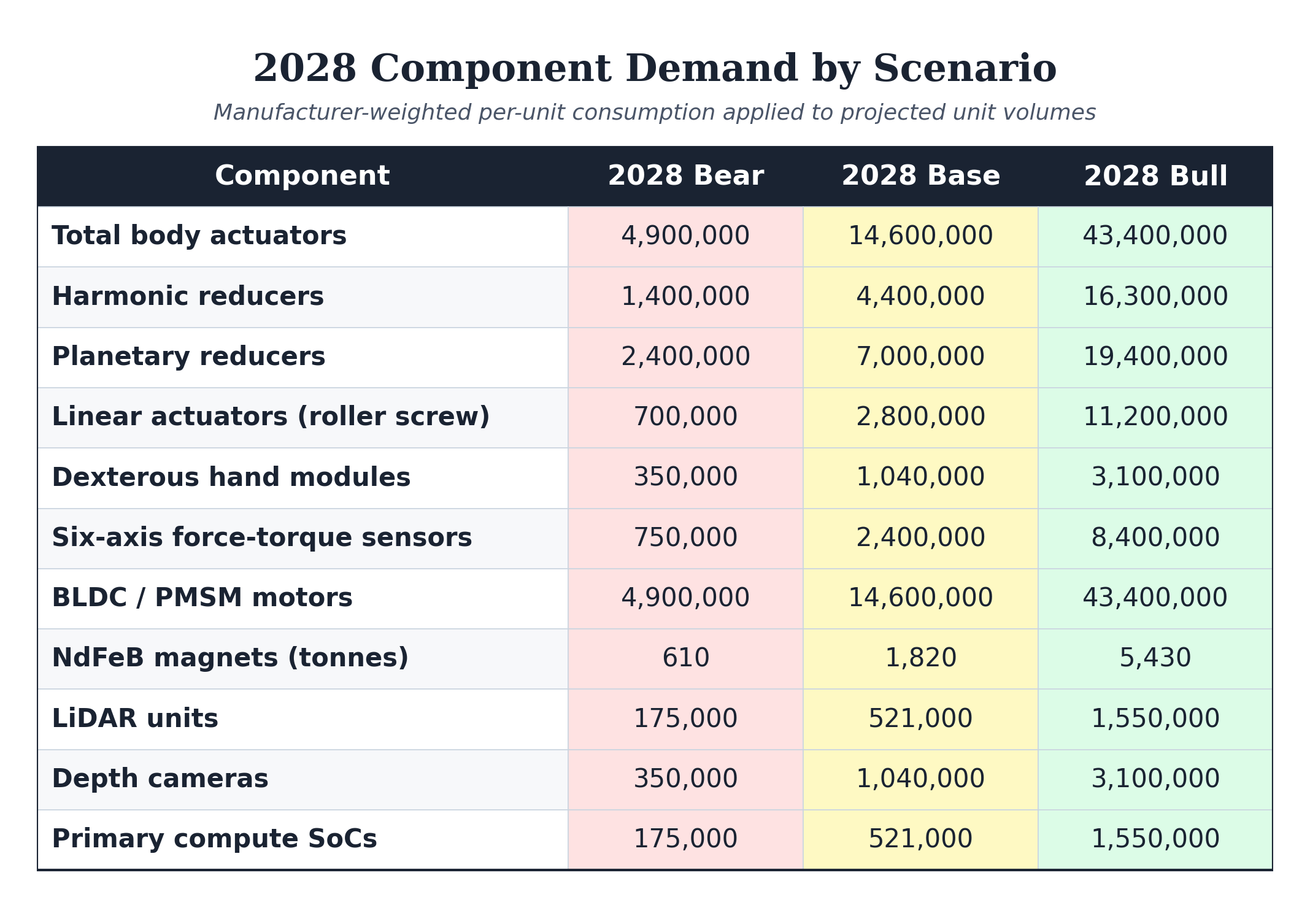

Projected Shipments & Component Demand

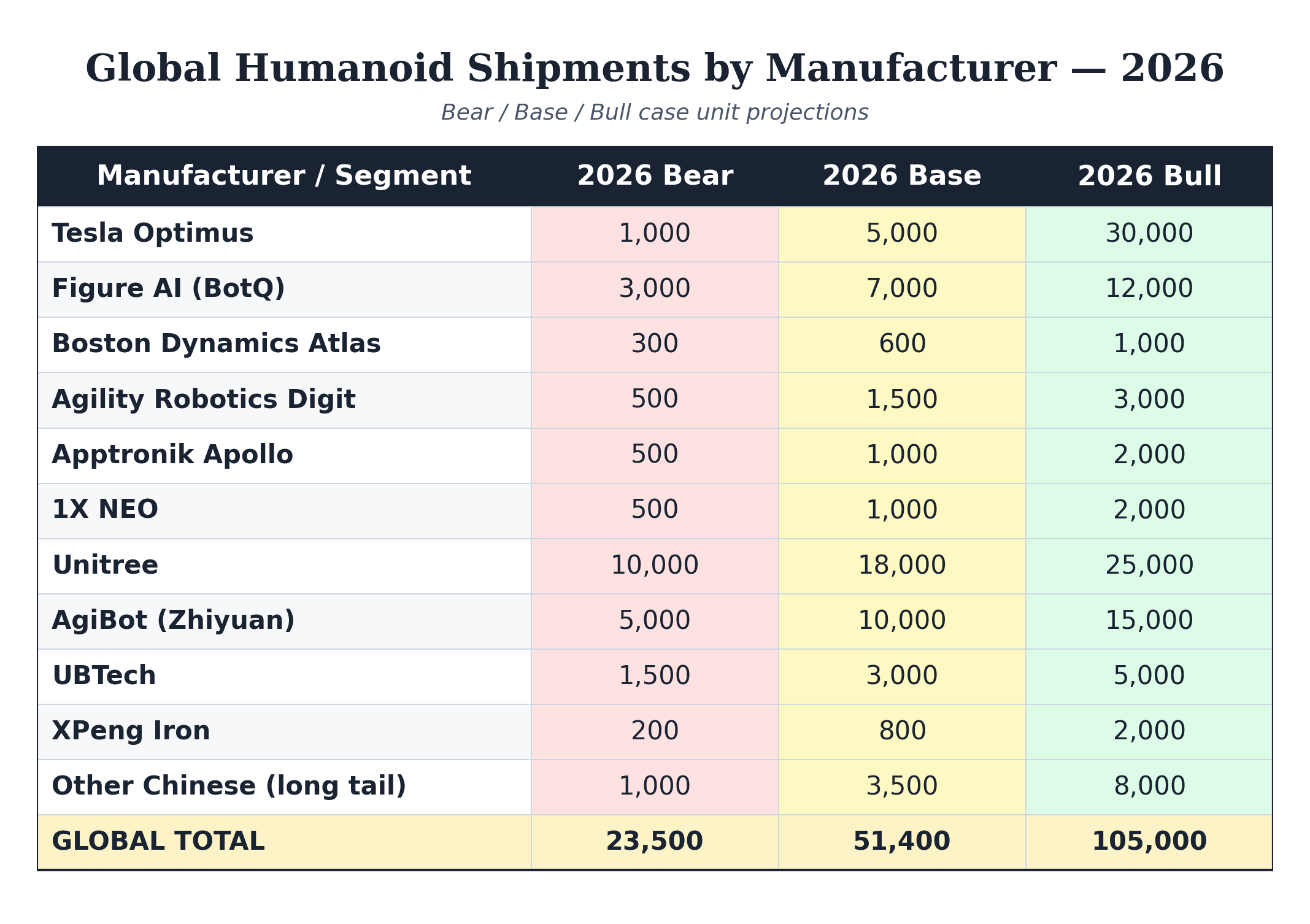

For 2026 projection, we anchor onto guidance given by companies and capex commitments and production line nameplates for the year 2026. This gives us a starting point to ascertain what could possibly happen if production runs smoothly with minimal iterations, forming the bull case.

For the base case, we account for humanoid manufacturing being a new endeavor and bound to face problems and reiterations. Thus a haircut of ~50% or in accordance with manufacturer-specific calibration. The manufacturer-specific calibrations are derived through historical guidance misses and self-discretion.

Finally, for the bear case a further ~50% haircut or in accordance to manufacturer-specific calibration is applied to base case to model structural conditions failing such as rare-earth magnet export controls intensifying and persistent execution problem.

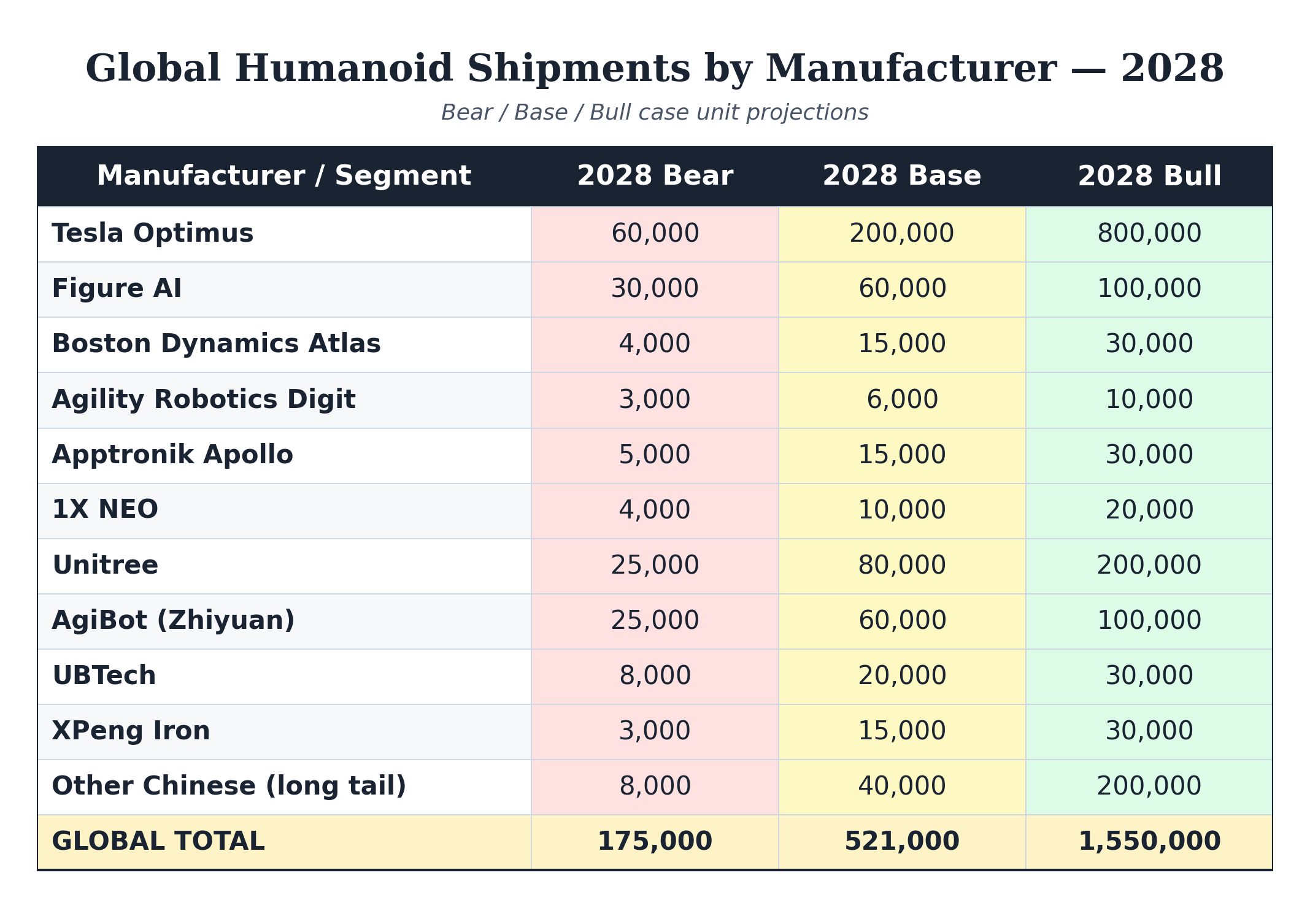

As for 2028 projections, the anchor shifts toward physical capacity. We looked at stated factory nameplates (Tesla Fremont 1M, Hyundai Georgia 30K, Figure 100K 4-year target, Agility RoboFab 10K) and long-term trajectory anchors from management (AgiBot 100K, Unitree extrapolated growth plus IPO-funded new facility) to form the starting point for the bull case, assuming announced capacity actually comes online.

Then in accordance to what was done for the 2026 projection, a haircut and manufacturer-specific calibration were done to estimate base and bear cases.

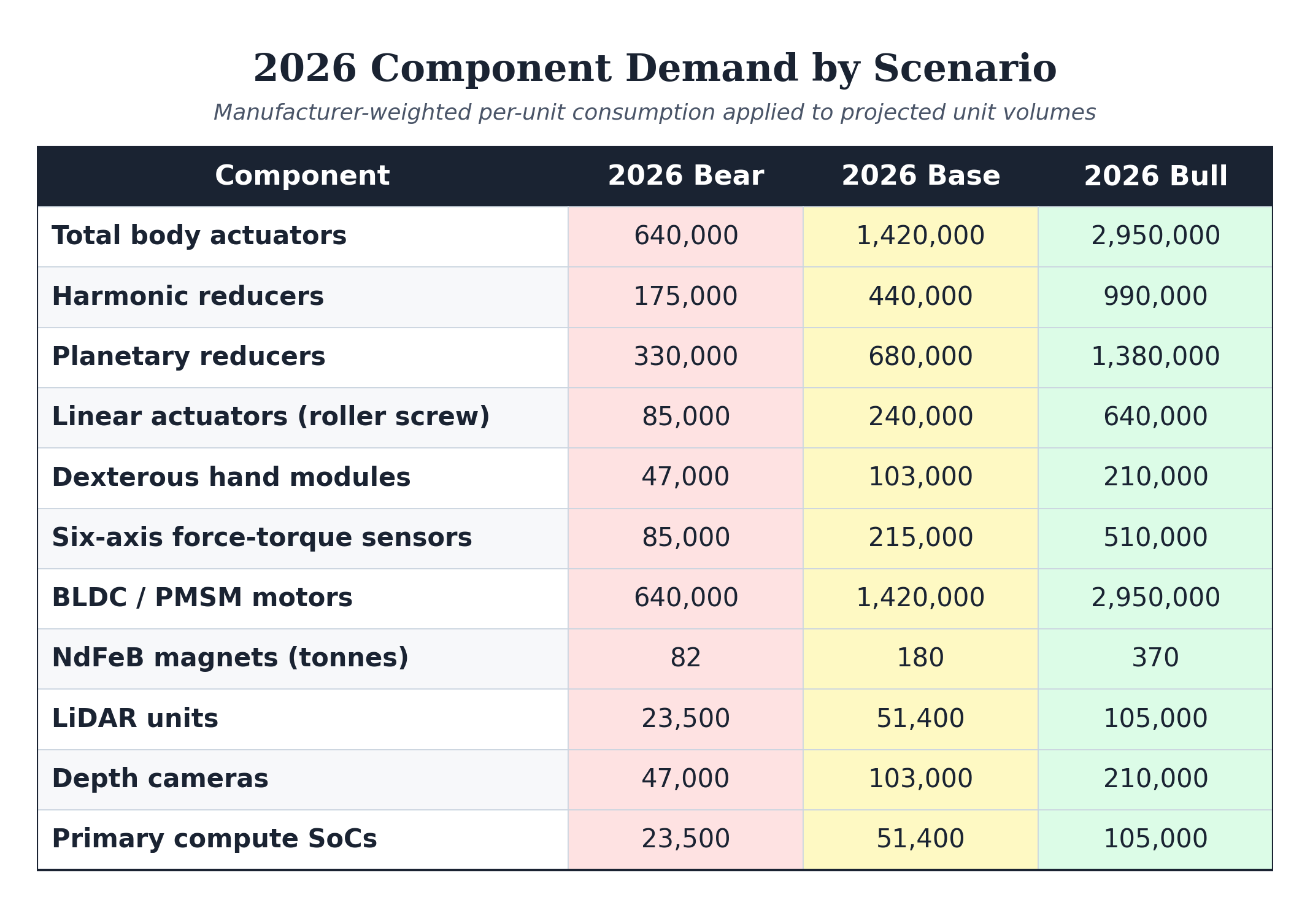

In the near term, demand for components is constrained by how many humanoid robots manufacturers can reasonably build and ship. For example, even in the bull case, manufacturers only consume an estimated 40% of current global harmonic reducer capacity.

In the long term, bottlenecks now bind in component supply. Once manufacturer capacity has been reasonably built out and software continues to improve leading to higher demand, the constraint moves upstream to whoever makes the actuators, reducers and magnets. 2028 base case alone exceeds current global harmonic reducer capacity by ~3x; bull case by ~13x.

Picks and Shovel Approach

The shift toward electric vehicles (EVs) has triggered one of the largest and most rapid industrial buildouts in history, characterized by a massive, global expansion of manufacturing capacity that rivals major technological transitions of the past. This boom, totaling hundreds of billions in investment, is not just rebuilding auto plants but creating an entire new supply chain, including gigafactories for batteries, raw material processing, and supporting infrastructure.

The deployment of such an immense number of humanoid robots would likely lead to an industrial buildout comparable in magnitude to the early EV wave.

Right now there are roughly a dozen credible humanoid manufacturers: Tesla Optimus, Figure, Agility, Apptronik, Boston Dynamics, 1X, Unitree, AGIBOT, UBTECH and a long tail behind them. The humanoid robot race, like historical technology races, will produce a graveyard. EVs had Tesla and BYD and a graveyard. Smartphones had Apple and Samsung and a graveyard. Yet, the component layer captures value regardless of which manufacturer survive, and within that layer five companies sit at the intersection of the highest BOM share, the most demanding precision manufacturing, and the smallest qualified supplier base globally.

Zooming Into Actuators

Elon Musk has said that actuators make up 56% of the bill of materials cost for Optimus. Humanoid robots are driven by motors which convert electricity into rotation. By itself, motors spin too fast with too little torque for the precision work that humanoid robots require.

Transmission is utilized to convert that fast, low-torque rotation into meaningful joint movement.

Harmonic reducers slow rotation way down and multiply torque. Tesla Optimus V3 utilizes frameless motors paired with harmonic reducers at shoulder joints and waist twist to create the huge torque needed to swing arms while carrying loads.

Quasi-direct drives (QDD) in Unitree G1 and H1 models use planetary gearboxes paired with high-torque-density frameless motors at every joint. The low ratio preserves backdrivability: external forces can push back through the gearbox, joints yield to impacts, and motor current alone tells the controller how much load the joint is carrying without a separate torque sensor. This is the architecture that makes parkour and dynamic movement possible.

Linear actuators using planetary roller screws convert motor rotation into linear push force. A frameless motor spins a threaded shaft inside the actuator housing; the screw drives a piston that extends and retracts to flex the knee, ankle, and hip.

Tendon drives take an anthropomorphic approach, mimicking human musculoskeletal anatomy. Tiny coreless motors spin small planetary gearboxes that wind cables onto spools. Cables run through the wrist and pull on individual finger joints which mimics how the tendon in our hands interact.

The four actuator types map cleanly to components:

QDD actuator = frameless motor + low-ratio planetary gearbox

Rotary actuator = frameless motor + harmonic reducer

Linear actuator = frameless motor + planetary roller screw

Tendon-driven actuator = coreless motor + small planetary gearbox + cable spool

The reason Tesla and Unitree use different actuators boils down to a single engineering tradeoff: gear ratio versus backdrivability. Both companies start with the same frameless motor technology. What differs is the transmission, and that choice cascades into nearly every other property of the robot.

High gear ratios, as in harmonic drives, give Tesla massive torque density and zero backlash - optimal for slow, precise, load-bearing tasks such as lifting, placing, holding position. The joint does not need to yield to impacts because Optimus is not running. The tradeoff is that high reduction ratios eliminate backdrivability. In other words, external forces cannot push back through the gearbox, so the controller cannot infer joint load from motor current alone. Tesla compensates with a dedicated torque sensor with each rotary actuator.

Low gear ratios, as in Unitree’s QDD architecture, sacrifice torque density for backdrivability and dynamic response. When the G1 lands a flip, every leg joint absorbs the impact rather than transmitting it rigidly into the frame. The cost is that the motor must actively generate holding torque continuously rather than relying on gearbox lock, requiring higher continuous current and a physically larger, magnetically denser motor.

The two architectures reflect two different bets on what humanoids will do for a living. Tesla is building for factory and household work dominated by slow, precise, load-bearing motions. Unitree is building for research and athletic deployment where dynamic motion is the entire point. Both bets are internally consistent. The supply chain consequences differ: Tesla’s harmonic-reducer-heavy, roller-screw-dense design creates specific, identifiable bottlenecks. Unitree’s QDD-dominant design is less exposed to the roller screw constraint but equally exposed to harmonic reducers and NdFeB magnets, since the frameless motors in QDD systems are magnetically intensive.

The Five Names

Pure humanoid bets

Suzhou Green Harmonic (688017.SH)

What they make. Harmonic reducers, the strain-wave gears that sit between the motor and the joint in every rotary actuator. Each humanoid (Optimus) uses roughly 14 of them across shoulders, elbows, wrists, hips, knees, and ankles. Harmonic reducers slow rotation down and multiply torque proportionally, allowing a small fast-spinning motor to drive a slow high-torque joint.

The qualification barrier. Harmonic reducers require special alloy steels for the flexspline (the elliptical-deforming component that gives strain-wave gears their name), ultra-precision tooth grinding, and high-performance flexible bearings that can withstand thousands of elliptical deformations per minute without fatigue failure over 20,000-plus operating hours. This makes qualification at industrial-grade precision for greenfield entrants roughly five years. Furthermore, the skilled labor pool is concentrated in Japan, China, and a few European specialty shops. Lastly, material qualification for the flexspline alloy alone takes 18 to 24 months.

The customer position. Green Harmonic holds roughly 30% of the Chinese domestic market and 15-25% globally, with humanoid revenue already at 30% of total revenue in Q1 2025. Tesla has identified Green Harmonic as the exclusive supplier on the harmonic line, with prices 30 to 40% below Japanese incumbent Harmonic Drive Systems. In addition, the 500,000-unit/year Suzhou plant ramping up in 2026 is the most concrete capacity disclosure in the entire space, dated and scoped against Optimus V3 mass production.

The catalyst. Suzhou plant increases production in 2026 and Optimus V3 ramp through 2026 to 2028.

The invalidation. If the 500K plant production slips or if Tesla redirects high-tolerance volume to Harmonic Drive Systems for premium applications, or if Tesla vertically integrates harmonic reducer production as it has done with other components historically, the thesis weakens materially.

The projection. 2026 Base: ~$34M | 2028 Base: ~$425M

Tesla exclusive on the harmonic reducer line for the Mexico factory plus ~30% Chinese domestic manufacturer share. Tesla 2026 Base (5,000 units) × 14 harmonic reducers per Optimus = 70,000 units. Chinese manufacturer 2026 Base (~34,000 units) weighted at ~6.5 harmonic reducers per humanoid (low-spec Unitree R1/G1 use ~5, mid/high-spec use ~10) × 30% share = ~66,000 units. Total ~136,000 reducers × $250 ASP (Chinese reducer-only pricing) = ~$34M.

For 2028, Tesla scales to 200,000 units (2.8M reducers) plus Chinese manufacturer reach ~215,000 units (~420,000 reducers captured at 30% share). Total ~3.2M reducers × $180 ASP (compressed) = ~$425M

Tuopu Group (601689.SH)

What they make. Complete rotary actuator assemblies for Optimus, integrating motor, harmonic reducer, encoder, sensor, and controller into finished units.

The qualification barrier. Integration is a different problem than component manufacturing. Each actuator design requires sub-micron alignment between motor and reducer, thermal management to prevent magnet performance breakdown, safety for human interaction, and torque density at the limit of current electromechanical design. It seems that Tesla and Tuopu have formed a co-development relationship rather than a vendor relationship, signifying a potential long-term alignment.

The customer position. Tesla revenue is 35 to 40% of Tuopu’s total business, company-disclosed. The relationship dates to 2016 when Tuopu became a Tesla Model 3 chassis supplier, which is the kind of decade-long integrated relationship that produces real co-development access. The Mexico factory 200 km from Giga Texas with 72-hour supply response time is the largest disclosed humanoid-specific capex commitment among Tesla suppliers. Hangzhou facility adding 200,000 unit/year capacity in Q1 2026, scaling to 3.5 million units total.

The catalyst. Q1 2026 capacity addition at Hangzhou. Optimus V3 mass production starting end-2026. Disclosed humanoid revenue in upcoming quarterly reports.

The invalidation. Tesla concentration in both directions. If Optimus volumes slip materially below current guidance, Tuopu’s revenue exposure is direct and large. If Tesla brings rotary actuator integration in-house the Tuopu relationship contracts.

The projection. 2026 Base: ~$84M | 2028 Base: ~$1.5B

For 2026 base case, revenue tracks Tesla Optimus volume directly with no other meaningful manufacturer exposure. Tesla 2026 Base (5,000 units) × 14 rotary actuators per Optimus × $1,200 ASP per full assembly = ~$84M.

For 2028, Tesla 200,000 units × 14 actuators × $550 ASP (compressed but not at Tesla’s most aggressive target) = ~$1.5B. Gross margin above 50% disclosed makes this the cleanest operating-leverage story of the five names, although revenue captured per Optimus is less than Wuzhou because rotary actuators are individually cheaper than linear actuator assemblies.

Wuzhou Xinchun (603667)

What they make. They make planetary roller screws for linear actuators that drive hip, knee, ankle, and forearm motion. Each Optimus uses 14 planetary roller screws at unit prices of roughly $1,350 to $2,700 each, representing approximately 19% of total robot BOM cost. Roller screws are one of the largest individual component bucket in the entire bill of materials.

The qualification barrier. Roller screws require precision grinding equipment and the grinding wheels and thread-cutting equipment are themselves precision instruments that take years to install and qualify. Heat treatment processes have to be controlled to maintain dimensional stability across thermal cycling. Thread grinders are mostly imported from Germany, Japan, and Switzerland, and domestic Chinese candidates to break that equipment chokepoint are early-stage. The industry simply cannot install new precision grinding capacity quickly.

The customer position. Wuzhou Xinchun entered Tesla’s supply chain in 2022 as a designated supplier of drive motor bearing races for North American car models. In March 2024. Wuzhou formed a Strategic Cooperation Framework Agreement with Hangzhou Xinjian Electric Drive to “indirectly supplying linear actuator components through partnership with Xinjian”. While Tesla currently sources planetary roller screws primarily from GSA Switzerland (RGTI 12.8 inverted planetary roller screw), Wuzhou pricing is roughly 50% of Swiss GSA pricing and Xinjian has been identified as the China qualifier for roller screws. Finally, its Thailand factory is reported to come online in 2026 serves as an essential geopolitically compliant logistics routes to North American gigafactories.

The catalyst. Thailand factory commissioning in 2026 to bypass geopolitical tariffs. Tesla volume ramp through V3 production.

The risk. Disclosure quality is thinner than for the Tesla actuator integrators. The relationship is reported through indirect sources rather than direct company filings. The “indirectly supplying linear actuator components through partnership with Xinjian” phrasing is two layers removed from a direct contract. If Tesla shifts toward ball screws to reduce costs in some joint positions (V3 patents shows some movement in this direction), demand mix could compress.

The projection. 2026 Base: ~$146M | 2028 Base: ~$2.6B

Tesla-tilted through direct supply chain qualification. Wuzhou entered Tesla’s North American supply chain in 2022 for drive motor bearing races, then deepened into roller screws via the March 2024 partnership with Hangzhou Xinjian Electric Drive - Tesla’s “China qualifier” for planetary roller screws.

Tesla 2026 Base (5,000 units) × 14 planetary roller screws per Optimus = 70,000 screws. + ~30% share of Chinese mid-tier manufacturers (AgiBot, UBTech high-end, XPeng Iron) adopting linear-actuator architectures, at ~6 roller screws each = ~11,000 additional screws. Total ~81,000 × $1,800 ASP (current low-volume Chinese pricing, ~50% below Swiss GSA) = ~$146M.

For 2028, Tesla 200,000 × 14 = 2.8M screws, plus Chinese share scaling to ~500,000 screws. Total ~3.3M × $800 ASP (compressed) = ~$2.6B.

Humanoid plus broader automation

Harmonic Drive Systems (6324.T)

What they make. The global reference supplier for harmonic reducers, having invented strain-wave gear technology decades ago. Roughly 35% global market share, declining versus Green Harmonic but still the specification reference for Western humanoid manufacturers and the existing industrial robotics base.

The qualification barrier. Same as for Green Harmonic. The five-year qualification timeline applies regardless of geography. Harmonic Drive Systems holds the technology IP advantage from being the original inventor, plus decades of refinement in flexspline alloy chemistry and tooth grinding precision that newer entrants are still catching up to.

The broader automation business. The bulk of the business comes from industrial robot arms (FANUC, ABB, KUKA, Yaskawa use 4 to 6 harmonic reducers per six-axis arm), collaborative robots (Universal Robots, Doosan, Techman, Fanuc CRX use harmonic reducers at every joint), semiconductor wafer handling robots (Brooks Automation, RORZE, Daihen), medical robotics (Intuitive’s da Vinci, Stryker’s Mako, Medtronic’s Mazor), and aerospace applications (satellite solar array drives, antenna pointing). The cobot market alone is growing roughly 20% annually, and HDS supplies essentially every cobot maker. If humanoids take longer to scale, HDS still has a real growth business in industrial automation.

The humanoid kicker. Reference supplier across the Western humanoid manufacturer cluster: Figure, Apptronik, Agility, Boston Dynamics. As these manufacturers ramp through 2026 to 2028, humanoid revenue layers on top of the existing industrial automation base. The bet is that the total reducer market grows fast enough that HDS can win on Western humanoid manufacturers even as it loses China share to Green Harmonic.

The catalyst. Figure, Apptronik, Agility, and Boston Dynamics all scaling Western humanoid production through 2026 to 2028. Industrial robot demand recovery. Cobot growth continuing at 20% per year.

The invalidation. Pricing pressure from Green Harmonic is real and ongoing. Global share has eroded from over 50% historically to approximately 35% today. If Chinese cost compression accelerates and Green Harmonic captures Western humanoid manufacturers through pricing, the HDS position weakens.

The projection. 2026 Base: ~$69M | 2028 Base: ~$950M

Western humanoid manufacturer reference supplier (Figure, Apptronik, Agility Digit, Atlas, 1X NEO). Sells the harmonic reducer component at Japanese premium pricing (~30-40% above Chinese suppliers like Green Harmonic). Western manufacturer 2026 Base (~15,500 units) × ~12 harmonic reducers per unit (mid-tier weighted) = ~186,000 reducers. In addition, residual ~5% Chinese manufacturers share on premium qualification-sensitive lines = ~11,000 reducers. Total ~197,000 × $350 ASP = ~$69M.

For 2028, Western manufacturer Base scales to ~306,000 units × 12 × $250 ASP (compression) = ~$920M, plus residual Chinese share of ~$30M = ~$950M. Against HDS total revenue of ~¥85B (~$565M), the 2028 humanoid number approaches the size of the entire current business. Keep in mind, the cobot kicker running underneath (Universal Robots, Doosan, FANUC CRX) provides a non-humanoid growth base independent of humanoid execution.

Hiwin Technologies (2049.TW)

What they make. A multi-component motion control specialist supplying ball screws, harmonic reducers, linear guideways, crossed roller bearings, torque motors, and integrated joint modules through subsidiary Hiwin Mikrosystem. The company is launching its own planetary roller screws in June 2026, extending coverage into the highest-specification linear motion category. Hiwin is one of only four Taiwanese firms in Morgan Stanley’s global top 100 humanoid robot suppliers, alongside TSMC, Foxconn, and Hota.

The broader automation business. Ball screws and linear guideways are the foundation business, used heavily in machine tools (CNC milling, grinding, EDM equipment) and semiconductor handling robots. The semiconductor capex cycle alone drives meaningful Hiwin revenue independent of humanoids. Hiwin supplies wafer transfer systems, single-axis robots, multi-axis SCARA robots for assembly lines, and medical equipment. The Dexterity collaboration on logistics warehouse robots adds an eight-axis logistics arm exposure that captures the automation buildout in warehousing and distribution beyond the humanoid form factor.

The humanoid kicker. Chairman Eddie Chuo has guided that robotics revenue will exceed 10% of group revenue in 2026. Hiwin is reportedly part of the Foxconn humanoid robot alliance and has already entered the dexterous hand supply chain for major US humanoid robot clients, with joint module samples under evaluation. Multi-manufacturer exposure rather than concentrated single-customer risk.

The catalyst. Planetary roller screw launch in 2026. Dexterity collaboration scaling beyond small-batch testing. Robotics revenue exceeding the 10% threshold that re-rates the diversified industrial business as a humanoid play.

The invalidation. Humanoid concentration is meaningfully lower than the Chinese pure-plays. 10% of revenue is real but it’s not 30% like Green Harmonic. The thesis depends on Hiwin successfully launching planetary roller screws against the entrenched Swiss-German duopoly. Hiwin is a diversified industrial name with a humanoid option attached, not a pure humanoid play.

The projection. 2026 Base: ~$8-10M | 2028 Base: ~$105M

Base 2026 capture: ~5% Western harmonic share (9,000 × $350 Japanese-equivalent Taiwan pricing = ~$3.2M) + ~10% Western dexterous hand modules (3,000 × $400 = ~$1.2M) + Foxconn alliance ball screws and guideways (~20,000 × $150 = ~$3M). Total ~$8-10M.

For 2028, the planetary roller screw launch matures into Tesla supply chain testing and the Foxconn humanoid alliance scales. Assume ~3% share of 2028 planetary roller screw demand (3.3M units × 3% = ~100,000 units × $700 ASP at Taiwan pricing post-compression) = ~$70M from roller screws + harmonic share scaling to ~$15M + foundation ball screws/guideways for Foxconn alliance and Dexterity logistics arms ~$20M. Total ~$105M humanoid-specific revenue. Hiwin is the smallest near-term but has the broadest 2028 ramp optionality due to their diversified industrial automation name with a humanoid kicker rather than a pure-play.

How the five fit together

Before walking through what each name uniquely captures, it’s worth being explicit about how the five fit into the broader manufacturer landscape.

Tesla has announced the largest disclosed capex commitment and a deliberately externalized supplier network. Its production timeline is also the most concrete in the space: V3 trial production is already underway, mass production is expected by end-2026, and the line is designed for one million units annually. That combination of scale, capital commitment, and willingness to outsource is exactly what makes Tesla the most tradeable manufacturer through its component suppliers. Green Harmonic, Tuopu, Wuzhou are direct Tesla supply chain plays.

Harmonic Drive Systems, Hiwin are in the basket because Tesla cannot be the entire thesis. Figure, Apptronik, Agility, Boston Dynamics, 1X, UBTECH, Agibot, and the broader Chinese humanoid cluster collectively matter, even if no single one of them matches Tesla on capex or timeline. Concentrating the entire bet on Tesla’s execution would be a single-manufacturer trade dressed up as a supply chain thesis. The diversified incumbents capture the non-Tesla manufacturer exposure and provide ballast against the scenario where Tesla slips and other manufacturers continue ramping.

There is a more important reframing of the time horizon worth making explicit. The market currently treats humanoid robots as a binary outcome: either humanoids ramp on the stated timeline and supplier stocks compound, or humanoids disappoint and the thesis fails. That framing misses the intermediate step. The realistic path is limited humanoid deployment now to collect real-world training data, AI-driven non-humanoid automation expanding in parallel, then humanoid scale-up as the data and models mature. The current production ramps from Tesla, Figure, and the Chinese manufacturers are deliberately small because the robots being built today are data collection platforms.

In the meantime, broader factory automation, cobot adoption, semiconductor handling, and warehouse logistics automation are all scaling now on AI-driven productivity gains, with revenue showing up in current P&L. The five-name basket captures both the near-term automation ramp and the longer-term humanoid scale-up because they are sequential parts of the same secular trend.

This is why the diversified incumbents matter. Harmonic Drive Systems and Hiwin benefit today from the AI-driven automation expansion happening across cobots, semiconductor capex, and warehouse logistics. They will benefit later from humanoid scaling when it arrives. The pure-plays (Green Harmonic, Tuopu, Wuzhou) are positioned for the humanoid scale-up specifically, which is the longer-dated leg of the trade. Holding both groups acknowledges that humanoid robots are a long-term play whose initial signs of life are showing up in early production ramps today, but the bridge to large-scale deployment runs through several years of AI-driven adjacent automation first.

With that, here is what each name uniquely captures.

Green Harmonic answers: who supplies the most cost-effective, and quality harmonic reducers to the Chinese supply chain and to Tesla? A single dominant Chinese player with 30% domestic share and disclosed Tesla exclusivity. Green Harmonic represents a pure-play humanoid bet.

Tuopu answers: who integrates rotary actuators for Tesla Optimus at scale? Likewise, Tuopu represents a pure-play humanoid bet.

Wuzhou answers: who supplies the most binding component bottleneck in the entire BOM? A Chinese roller screw maker positioned at the top of the qualified Chinese supplier hierarchy, supplying Tesla through both direct relationships and the broader Optimus supply chain network.

Harmonic Drive Systems answers two questions at once: what if Tesla isn’t the only manufacturer that matters, and Western humanoid manufacturer win meaningful share? What if humanoid takes a longer runway but the industrial robot, cobot, semiconductor wafer handling, and medical robotics markets keep growing? The global incumbent reference supplier captures both scenarios, with humanoid as the upside option on top of a defensible industrial automation business.

Hiwin Technologies answers: who captures multi-component value as the humanoid industry diversifies its supply chain across geographies and architectures, while also benefiting from the semiconductor capex cycle, machine tool demand, and warehouse automation buildout? A Taiwanese motion control specialist with the broadest product coverage, the most diversified humanoid customer base, and meaningful non-humanoid automation exposure.

Future Direction

This basket is the entry point to investing in the humanoid robotics and robotic automation supply chain, not the full map. Subsequent pieces will dig into rare earth magnets as the next binding constraint upstream, and into each of these five names individually with the depth they deserve.